Consultant vs. Operator: The Great Debate in PE Operating Partner Hiring

Consultant vs. Operator: The Great Debate in PE Operating Partner Hiring

The most important talent decision in private equity isn’t who leads the next deal—it’s who you hire as operating partner. With 47% of PE value creation now from operations (Accenture), getting it wrong means expensive misfires: consultants who never execute, or operators who alienate management (Umbrex.)

Financial engineering’s role in returns has collapsed (from 51% in the 1980s to 25% today Wall Street Prep), while PE dry powder has swelled to $2.62 trillion AlphaSense. With assets trading at 12–15x EBITDA Heidrick & Struggles, funds must build value through operations—and the right talent model decides who wins.

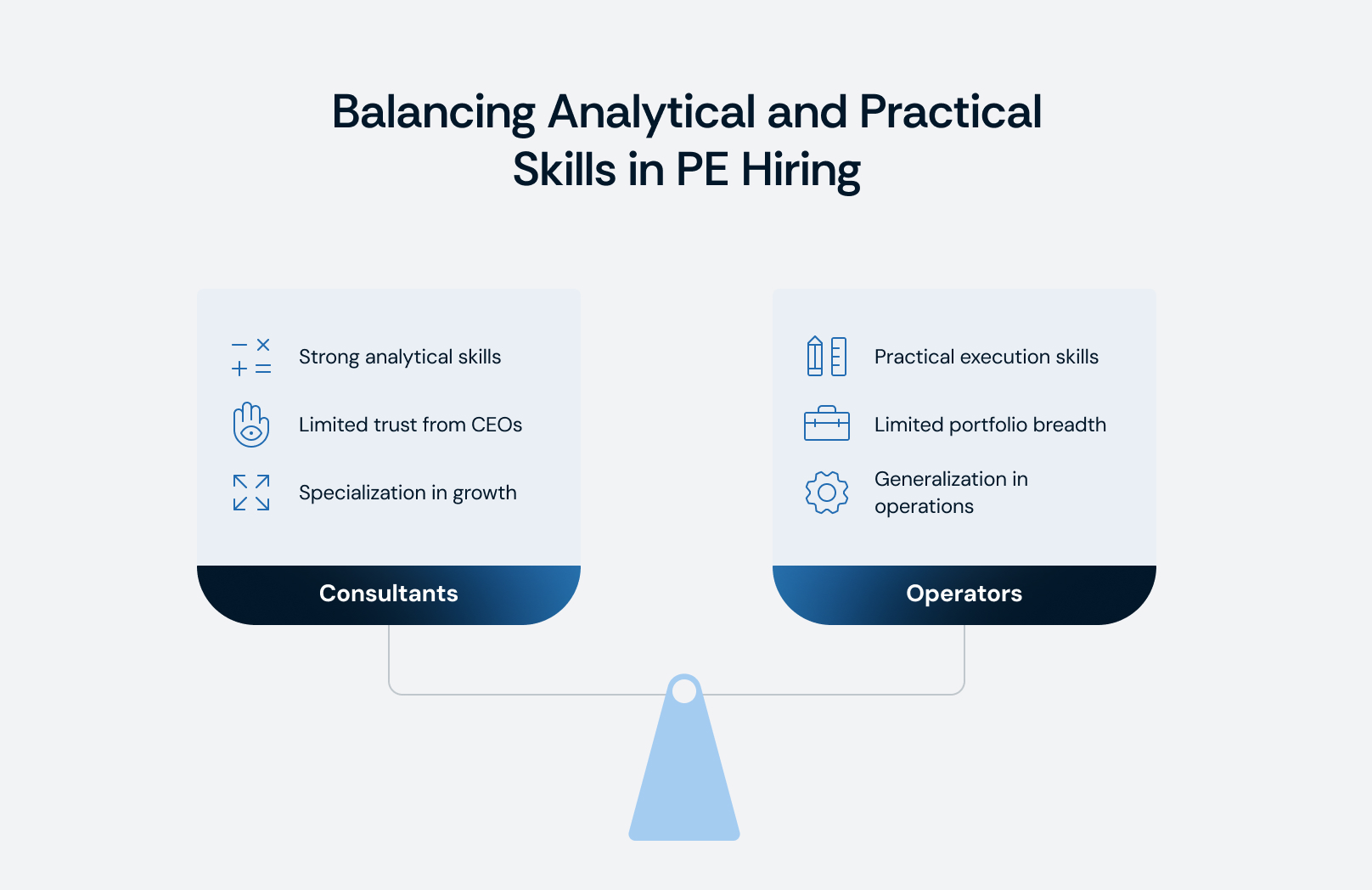

Consultants: Brilliant Analysts, Weak Executors

The upside:

- MBB consultants bring unmatched analytical rigor, frameworks, and commercial due diligence skills Growth Equity Interview Guide.

- At KKR Capstone, 10 of 11 MDs are ex-consultants, 6 from McKinsey Umbrex.

- Consultants excel in 100-day planning, pricing, and sales effectiveness—high-leverage work that can swing returns ListAlpha.

The downside:

- Consultants struggle with implementation—firing execs, restructuring factories, or union negotiations KKR.

- Portfolio CEOs often see them as outsiders or “spies for the fund” Egon Zehnder.

- Many burn out quickly in PE’s execution-first culture, with high churn back to consulting Wall Street Oasis.

Where they work best: growth equity, carve-outs, SaaS, and playbook-driven initiatives requiring structured analysis.

Operators: Trusted Executives, Limited Breadth

The upside:

- Former CFOs, COOs, and divisional presidents bring hard-earned credibility—they’ve owned P&Ls, built teams, and run crises Amazon.

- CEOs trust them as peers; they excel in hands-on transformations, talent recruiting, and turnarounds Axial.

- Their networks provide access to sector talent and suppliers consultants can’t match Umbrex.

The downside:

- Many “operators” lack true operating depth—title inflation masks experience gaps Heidrick & Struggles.

- They often struggle with portfolio breadth and context-switching, preferring deep engagement over rapid pivots PwC.

- “Star hires” (e.g., Jack Welch at CD&R) often deliver LP sizzle but little real work CAIA.

Failure mode: overconfidence leading to overpaying for distressed assets, misjudging CEOs, or optimizing for short-term metrics that backfire (e.g., KKR/Envision Healthcare surprise billing scandal) Yale.

The Assessment Challenge

Unlike deal pros, operating partners lack clean metrics (like IRR attribution). Soft skills—influencing CEOs, balancing deal team dynamics—matter more than resumes Egon Zehnder.

Best practices:

- Define role expectations clearly (strategic advisor vs. interim exec vs. functional expert) Accordion.

- Use back-channel references early, framed as “how to set them up for success” Lock 8 Partners.

- Run real-world simulations: have candidates build a 100-day plan or walk through an EBITDA improvement.

- Evaluate influence with both deal partners and portfolio CEOs—not just technical ability.

The Optimal Mix: Complementary Teams

The right answer isn’t consultant vs. operator—it’s both.

- KKR Capstone leans consultant-heavy but organizes into functional Centers of Excellence ListAlpha.

- Vista Equity Partners runs a 1:1 ops-to-deal team ratio, with a prescriptive 100+ point playbook and internal “Vista University” Umbrex.

- Blackstone emphasizes functional expertise (data, AI, cybersecurity, procurement) Blackstone.

Pattern: consultants drive analytics and strategy; operators drive implementation and CEO trust. Together, they multiply value.

The Rise of Specialists

Despite generalists earning ~14% more Charles Aris, demand is shifting to specialists:

- AI & data: fastest-growing role, central to deal assessment and post-close optimization Korn Ferry.

- ESG: funds with strong ESG practices achieve up to 8% higher IRR Deloitte.

- Digital transformation, pricing, supply chain: increasingly essential for value creation.

Sector context drives profile choice:

- Tech & SaaS: consultant-heavy (pricing, growth, analytics).

- Industrial & manufacturing: operator-heavy (lean, supply chain, floor management).

- Healthcare: hybrid (regulatory operators + digital consultants).

- Consumer/retail: shifting to consultants with digital and omnichannel expertise.

The Future: Hybrids & AI-Enabled Ops

The best talent increasingly has both backgrounds: 4–6 years at McKinsey + 3–5 years as COO/divisional head, returning to PE as hybrids Heidrick & Struggles.

AI is now table stakes: 70% of M&A execs believe generative AI can boost returns Accenture. Operating partners must drive AI deployment in manufacturing, healthcare, consumer, and services—or risk irrelevance.

Integration Is the Real Differentiator

The consultant vs. operator debate matters less than how firms structure the role.

- Are ops partners in the IC from diligence onward—or pulled in post-close?

- Do they have carry equal to deal pros—or just fee-based comp?

- Are they given authority and board seats—or sidelined as advisors?

The winners (Vista, KKR, Bain, Blackstone) treat operating partners as first-class citizens. The laggards hire for LP optics, undercompensate, and exclude ops from decision-making—burning capital while competitors compound operational alpha.

Bottom Line

Hiring the wrong profile wastes millions; hiring the right one compounds advantages for decades. The consultant vs. operator divide is real, but the firms that win:

- Blend both skill sets strategically.

- Specialize where needed (AI, ESG, digital, supply chain).

- Integrate ops into deal processes with authority, carry, and IC seats.

Operational alpha now drives nearly half of PE returns. The firms that build genuine, integrated operating platforms will dominate fundraising, deal execution, and exits. Those clinging to outdated models will fall behind—regardless of whether they hired a McKinsey EM or a former divisional CFO.