The Operating Partner Talent War: Where to Find Candidates When Everyone Is Hiring from the Same Pool

Private equity is scaling. The talent pipeline isn’t.

The global PE market has surged from $4.7T in 2021 to a projected $6T in 2024. Operational value creation now drives 47% of returns, up from just 18% in the 1980s. But the supply of qualified operating partners—who turn strategies into EBITDA—isn’t keeping up.

The result? A 3–10X supply-demand gap that’s fueling a bidding war for a narrow, overstretched talent pool. Compensation is spiking. Searches now stretch up to 180 days. And still, most firms are chasing the same candidates—with increasingly diminishing returns.

The numbers are stark:

- Only 27% of current operating partners come from consulting.

- McKinsey, Bain, and BCG produce just ~3,000 hires/year—and only a fraction become PE-ready.

- Meanwhile, 76% of PE firms say talent acquisition is now a top priority.

The traditional MBB pipeline? Insufficient. In 2023, Bain and BCG paused MBA hiring. McKinsey tightened performance reviews to quietly trim headcount. And all this as 81% of PE executives say they’re holding investments longer than planned—making operational talent not just helpful, but existential.

The war for operating talent isn’t theoretical. It’s now. And firms still fishing in the same waters will lose deals, LP confidence, and market position to those who’ve found where the real talent is hiding.

The Current Talent Crisis: A Market Fundamentally Out of Balance

The operating partner shortage isn’t cyclical—it’s structural. As private equity scales, the gap between demand and qualified talent widens every quarter.

The numbers make it plain. In 2024, Heidrick & Struggles and Private Equity International surveyed just 251 and 314 operating executives, respectively—sample sizes that underscore just how constrained the pool is. Meanwhile, thousands of PE firms globally require anywhere from 2 operating execs (sub-$500M funds) to 28+ (mega-funds over $20B AUM). The math doesn’t work.

What’s Driving the Demand?

Put simply: the model has shifted. Since 2010, operational improvement has driven 47% of PE value creation, while financial engineering has dropped to just 25%—a complete reversal from the 1980s, per PwC’s 2024 analysis. And with leverage more expensive, multiples compressed, and exits stalled, there’s no fallback. Operational capability is no longer a competitive edge—it’s survival.

LPs see this clearly. As of mid-2024, $2.62T in dry powder sits idle while deal activity hit its lowest levels since 2016, per PitchBook. They’re no longer accepting vague value creation plans—they want evidence of proven operating firepower before committing capital.

The Cost of Delay

Time-to-fill is dragging down performance. According to Bespoke Partners, portfolio-level leadership roles now average 180 days to fill. That’s for P&L hires—fund-level operating roles take longer. Even the best search firms only cut that to 100 days. In a process where deals are won or lost on the strength of the ops bench, that’s too slow.

The outcome? Firms with robust talent pipelines are executing faster. Everyone else is stuck in gridlock.

Compensation Is Climbing—But It’s Not Solving the Problem

Despite a 25–30% drop in search volume in 2024, Bespoke reports compensation has continued rising—a paradox that reflects structural scarcity, not soft demand.

Heidrick & Struggles puts today’s operating partner comp at:

- $180K–$2M base

- $200K–$1.75M bonus

- $323K–$25M+ in carry, depending on fund size

Yet even with 45.4% of execs reporting salary increases and 62.4% getting bonus bumps this year, the supply problem persists. The issue isn’t willingness to pay—it’s that qualified candidates are increasingly impossible to find.

The Cannibalization Loop

One signal says it all: 21% of operating partners in 2024 came from other PE firms, up from just 7% in 2022. That’s a 200% increase in intra-industry poaching—a clear sign of a broken external pipeline. Firms aren’t building talent—they’re raiding each other.

No Firm Size Is Immune

- Mega-funds ($20B+ AUM): Need 22–28 operating partners. Even with brand advantage, constant hiring is required.

- Mid-market ($3B–$5B): Need 14–16. Recruiting is harder without big-name pull.

- Lower-mid ($1.6B–$3B): Need 8–9. Often rely on part-time advisors—an increasingly unacceptable answer for LPs.

No matter the size, the talent crisis is the same: demand is relentless, supply is stagnant, and every firm is battling uphill.

The Over-Fished Talent Pool: Why MBB Isn’t the Answer Anymore

For decades, McKinsey, Bain, and BCG have been private equity’s default talent well. That’s the problem.

Everyone’s fishing in the same pond—and the pond is drying up.

The Numbers Don’t Add Up

At peak, the MBB firms hired ~3,000 people globally per year:

- McKinsey: 38.4%

- BCG: 37.3%

- Bain: 24.3%

That was during the 2020–2022 boom. Since then, hiring has reversed:

- BCG canceled MBA cycles in Fall 2022 and Fall 2023.

- Bain followed in Fall 2023.

- McKinsey is quietly downsizing via stricter performance reviews.

Even in boom years, this pipeline was too small. PE needs 500–1,000+ new operating partners annually. MBB may yield 100–200 qualified candidates at best. That’s a 3–10X mismatch.

The deeper issue? MBB may not be the right fit for what operating partners are now expected to do.

Smart ≠ Ready

Most MBB consultants spend 2–3 years post-MBA working on short, high-level strategy projects. They advise; they don’t execute. Operating roles in PE require the opposite:

- Ownership of P&Ls

- Decisive action under pressure

- Influence without authority

- Willingness to make hard calls in ambiguous environments

According to a survey of 700 execs, only 13% said MBB consultants on transformation projects “did more good than harm.” The rest either saw no impact—or negative impact.

It’s not a matter of intellect. It’s a matter of exposure. Execution is learned in the field, not in a deck.

Patterned Failure Modes

- Execution gaps: Great slides, no follow-through

- Financial blind spots: Shallow exposure to debt or capital structures

- Analysis paralysis: When PE needs action, consultants want another sprint

- Weak leadership muscle: They’ve advised CEOs, not led teams through resistance

- Cultural friction: PE rewards clarity and speed; MBB rewards consensus

Market Dysfunction: Scarcity → Bidding Wars

Despite these limitations, demand hasn’t eased. Firms now recruit 18+ months ahead, compressing offers into August–October frenzies.

- Vista runs 8-hour Super Days ending with same-day offers.

- JPMorgan and Goldman threaten 2025 analysts with termination for early acceptance of PE offers.

Comp is ballooning:

- For MBB managers (earning ~$300K–$400K): offers now start at $350K–$500K base + $200K–$350K bonus + carry

- For partners (earning $1M–$5M+): $650K–$900K base + bonuses + $2M–$5M+ in carry

Who Places Where

- Bain leads in middle-market PE due to its Private Equity Group.

- McKinsey dominates at mega-fund level.

- BCG lags due to thinner PE exposure.

But even top consultants need seasoning. The best operating partners with MBB pedigrees tend to succeed after 3–5 years in actual operating roles post-consulting.

The Smarter Play

MBB is still a valid signal—but no longer the source. Smart firms are widening the aperture: toward operators, P&L owners, and sector execs with executional depth and better cultural fit. And they’re finding those people outside the spotlight—where competition is lower and readiness is higher.

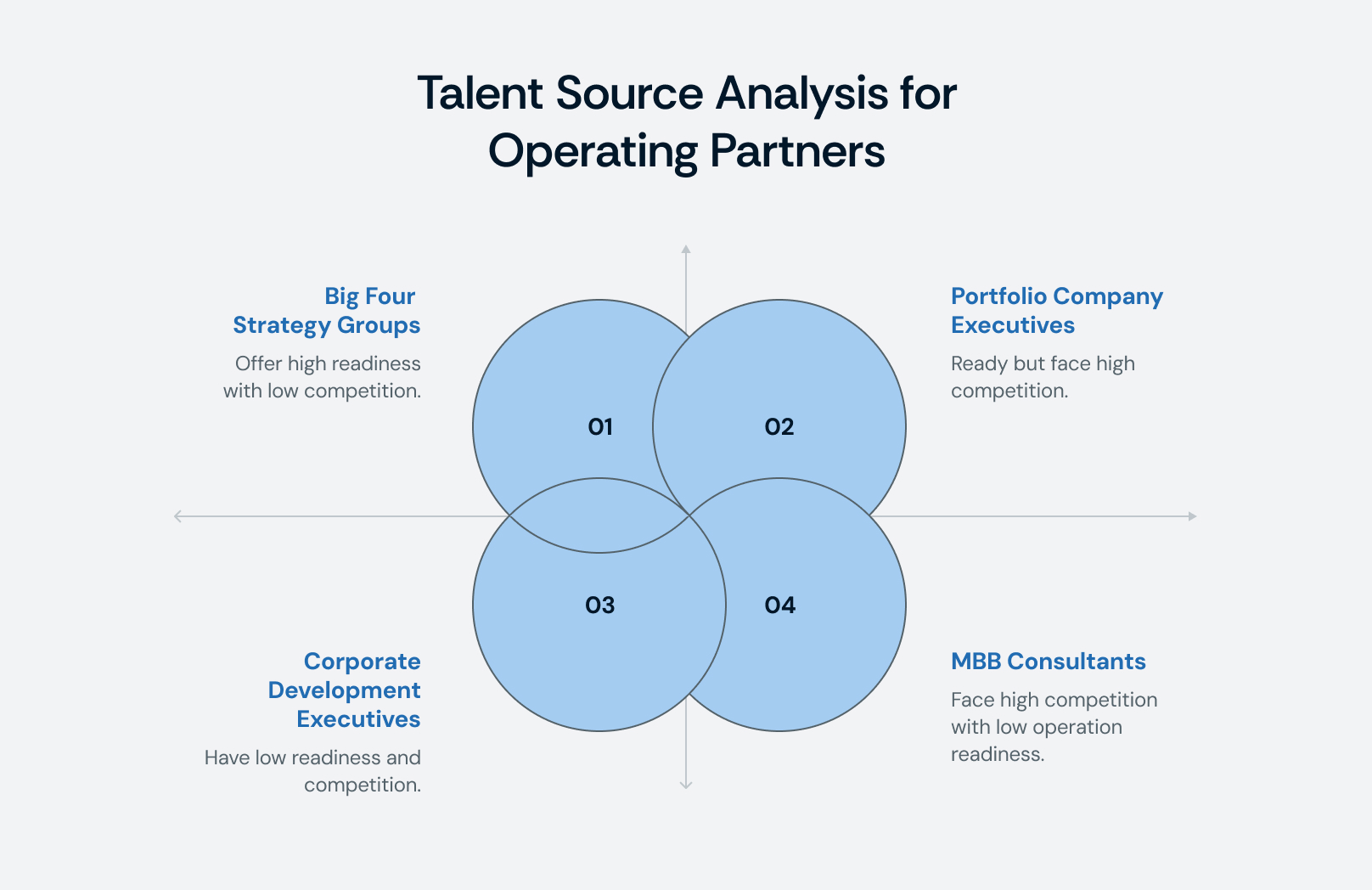

Overlooked Talent Sources Delivering Immediate Value

While mega-funds bid up McKinsey partners, a wide universe of operationally seasoned talent remains drastically underutilized. These overlooked pools offer deeper hands-on experience, more reasonable compensation expectations, and less competition.

Big Four Strategy Groups: Arbitrage in Plain Sight

Firms like EY-Parthenon, Monitor Deloitte, Strategy& at PwC, and KPMG GSG often fly under the radar—but they offer real value. For example, EY-Parthenon has 160+ partners with MBB experience, and together with L.E.K., they execute 400+ PE diligence projects annually—comparable to any MBB PE group.

Unlike MBB's 3-week sprints, Big Four consultants often embed for 6+ months, building deep operational context. EY-Parthenon excels in PE diligence; Monitor Deloitte in digital transformation; Strategy& in financial services. Despite the bias, these professionals often deliver stronger results at 30-40% lower compensation levels.

Mid-market firms are catching on. An EY-Parthenon alum shared: "I didn’t just recommend vendor consolidation—I negotiated contracts and delivered $12M in savings."

Boutique Consultancies: Deep, Targeted Expertise

Boutiques like L.E.K., Oliver Wyman, Kearney, Putnam, and Clarkston Consulting offer sector-specific depth MBB generalists can’t match. For instance:

- Putnam focuses exclusively on life sciences.

- Kearney is strong in manufacturing and supply chain.

- Roland Berger leads in European industrials.

These consultants bring pattern recognition from dozens of focused projects. And at 20-30% less cost than MBB peers, they often outperform on impact-per-dollar.

Corporate Development Executives: Operators in Disguise

Fortune 500 corporate development professionals offer real-world deal, integration, and P&L experience—but are rarely targeted. These are VPs/SVPs who’ve led billion-dollar transactions and driven value creation firsthand.

Recent shifts show firms becoming more open to operators without PE pedigrees. Compensation must be right, but the pitch is compelling: influence across multiple portfolio companies, faster liquidity through carry, and broader impact.

Portfolio Company Executives: PE-Tested, Ready to Scale

Executives who’ve already delivered in PE environments are often overlooked. They’ve executed 100-day plans, scaled EBITDA, and exited successfully. Their fluency in PE dynamics and ability to build high-trust relationships with boards make them low-risk, high-impact candidates.

Yet only 12% of current operating partners come from portfolio companies—a drop from 27% in 2022. This is a missed opportunity. Every successful exit generates multiple potential OPs.

Sector Specialists: Premium Results, Predictable Returns

As sector specialization increases, demand for industry-specific OPs has surged. Specialists command 15-25% premiums for good reason:

- Manufacturing: Lean experts deliver fast EBITDA gains.

- Software: Vista, Thoma Bravo, and Silver Lake have institutionalized sector-focused ops models.

- Healthcare: Specialists navigate reimbursement, labor costs, and clinical operations.

Cambridge Associates reports specialists delivering 340-940bps higher IRR vs. generalists. Their sourcing, execution, and exit edge makes the premium well worth it.

Deal Team Transitions: Hidden Talent Within

PE deal professionals increasingly shift to ops roles—bringing financial literacy, firm fluency, and deep portfolio knowledge. Firms like KKR and Bain Capital have internalized this with Capstone and Portfolio Groups.

These transitions work best when operators already show aptitude for influencing without authority and a genuine interest in execution. The result: low integration risk, high firm fit, and continuity across the deal lifecycle.

Overlooked Talent Sources Delivering Immediate Value

While mega-funds bid up McKinsey partners, a wide universe of operationally seasoned talent remains drastically underutilized. These overlooked pools offer deeper hands-on experience, more reasonable compensation expectations, and less competition.

Big Four Strategy Groups: Arbitrage in Plain Sight

Firms like EY-Parthenon, Monitor Deloitte, Strategy& at PwC, and KPMG GSG often fly under the radar—but they offer real value. EY-Parthenon has 160+ partners with MBB experience, and together with L.E.K., they execute 400+ PE diligence projects annually—comparable to any MBB PE group.

Unlike MBB's 3-week sprints, Big Four consultants embed for 6+ months, building deep operational context. EY-Parthenon excels in PE diligence; Monitor Deloitte in digital transformation; Strategy& in financial services. Despite the bias, these professionals often deliver stronger results at 30-40% lower compensation levels.

Mid-market firms are catching on. An EY-Parthenon alum shared: "I didn’t just recommend vendor consolidation—I negotiated contracts and delivered $12M in savings."

Boutique Consultancies: Deep, Targeted Expertise

Boutiques like L.E.K., Oliver Wyman, Kearney, Putnam, and Clarkston Consulting offer sector-specific depth MBB generalists can’t match. For instance:

- Putnam focuses exclusively on life sciences

- Kearney leads in manufacturing and supply chain

- Roland Berger dominates European industrials

These consultants bring pattern recognition from dozens of focused projects. At 20-30% less cost than MBB peers, they often outperform on impact-per-dollar.

Corporate Development Executives: Operators in Disguise

Fortune 500 corporate development professionals offer real-world deal, integration, and P&L experience—but are rarely targeted. These are VPs/SVPs who’ve led billion-dollar transactions and driven value creation firsthand.

Recent shifts show firms becoming more open to operators without PE pedigrees. The pitch is compelling: influence across multiple portfolio companies, faster liquidity through carry, and broader impact.

Portfolio Company Executives: PE-Tested, Ready to Scale

Executives who’ve already delivered in PE environments are often overlooked. They’ve executed 100-day plans, scaled EBITDA, and exited successfully. Their fluency in PE dynamics and ability to build high-trust relationships with boards make them low-risk, high-impact candidates.

Yet only 12% of current operating partners come from portfolio companies—a drop from 27% in 2022. This is a missed opportunity. Every successful exit generates multiple potential OPs.

Sector Specialists: Premium Results, Predictable Returns

As sector specialization increases, demand for industry-specific OPs has surged. Specialists command 15-25% premiums for good reason:

- Manufacturing: Lean experts deliver fast EBITDA gains

- Software: Vista, Thoma Bravo, and Silver Lake have institutionalized sector-focused ops models

- Healthcare: Specialists navigate reimbursement, labor costs, and clinical operations

Cambridge Associates reports specialists delivering 340-940bps higher IRR vs. generalists. Their sourcing, execution, and exit edge makes the premium well worth it.

Deal Team Transitions: Hidden Talent Within

PE deal professionals increasingly shift to ops roles—bringing financial literacy, firm fluency, and deep portfolio knowledge. Firms like KKR and Bain Capital have internalized this with Capstone and Portfolio Groups.

These transitions work best when operators already show aptitude for influencing without authority and a genuine interest in execution. The result: low integration risk, high firm fit, and continuity across the deal lifecycle.