The New Operating Partner: How AI, Data Science, and Technology Expertise Became Non-Negotiable

- Technology, especially AI and data science, has become essential to private equity value creation.

- Traditional operating partners are being replaced by tech-native leaders with deep technical skills.

- Top firms like Blackstone and Apollo treat technology as core, integrating it at partner level with full deal lifecycle involvement.

- Tech OPs drive 5–25% EBITDA gains—on par or better than traditional levers like procurement and pricing.

- LPs now require clear evidence of tech capabilities or reduce commitments.

- Firms without real tech infrastructure are falling behind; those investing aggressively are pulling ahead fast.

Private equity is undergoing a historic shift in what it values in operating partners. Today, it’s not just about strategy or general operations—it’s about technology. Data scientists, AI leaders, and digital transformation experts now command near-investment partner compensation, receive GP status, and drive value creation at a level traditional backgrounds can’t match.

The change is quantifiable: only 17% of operating partners had CEO experience in 2024 (down from 26% in 2022), while technology specialists now make up the largest single category at 19% (PEI). Firms systematically deploying AI are seeing 5–25% EBITDA gains (FTI)—results that dwarf traditional operational levers.

This isn’t a trend—it’s a full redefinition of value creation. With 79% of PE value now tied to operations (Accenture, PwC) and 95% of firms planning to increase AI investments over the next 18 months (DFIN, Korn Ferry), tech capability is no longer optional—it’s decisive.

The pressure is external, too. LPs now scrutinize firms’ digital operating capabilities in diligence. Sellers favor buyers who bring sophisticated tech playbooks. Portfolio company leaders want owners who can guide real transformation—not just give advice.

And the war for top-tier tech OPs? Fierce. Recruiters call it the most competitive talent environment in decades. The firms winning are those that embraced this shift early—and are now pulling away from those clinging to legacy models.

Technology-Native vs. Technology-Curious: Why Traditional Profiles No Longer Cut It

The collapse of the traditional operating partner model wasn’t gradual—it was swift and absolute.

From 2022 to 2024, the percentage of operating partners with prior experience at a portfolio company dropped from 27% to 12%. Former CEOs? Down from 26% to 17%. Meanwhile, hires with prior PE operating experience tripled, rising from 7% to 21%—a clear signal that firms are poaching proven talent, not training up corporate generalists (Heidrick & Struggles).

Functionally, tech now leads. In 2024, technology specialists made up 19% of all OPs—more than sales (15%), marketing (14%), or finance (14%) (PEI). That’s a full inversion of the legacy model, where broad C-suite generalists dominated. Today, depth in a mission-critical function beats breadth across peripheral ones.

Why the shift? Because traditional backgrounds can’t meet the moment.

As PwC put it: “The business transformation required to unlock value needs nuance and a level of domain knowledge traditional managers typically do not have.” Former CEOs and COOs may know strategy, but they often lack the technical fluency required to build modern operating models.

The gaps are decisive:

- No experience with software development lifecycles

- No ability to assess data architecture or analytics frameworks

- No credibility with engineering teams or vendor evaluations

- No firsthand exposure to AI, cloud, or cybersecurity governance

They can spot problems—but not solve them. That means reliance on costly consultants, slower execution, and missed opportunities that a technology-native OP would own end-to-end.

This isn’t just about skills—it’s about survival. Operational improvements now drive 79% of value creation. Financial engineering contributes just 25%—down from 51% in the 1980s. With exit multiples down, rates up 500+ bps, and leverage constrained, firms must win on execution—or fall behind (EY, Harvard Law School Forum, McKinsey).

As Granger Reis put it: “The days of buying low, leveraging high, and selling higher are over.” PE’s playbook has changed—and firms still staffing OP benches with legacy profiles are playing the wrong game.

The Rise of the Tech and AI Operating Partner

Technology operating partners have gone from niche to non-negotiable—and in 2024–2025, they’ve reached full parity with investment partners at leading PE firms (Korn Ferry). This isn’t a passing trend. It’s a structural shift reshaping how private equity creates value.

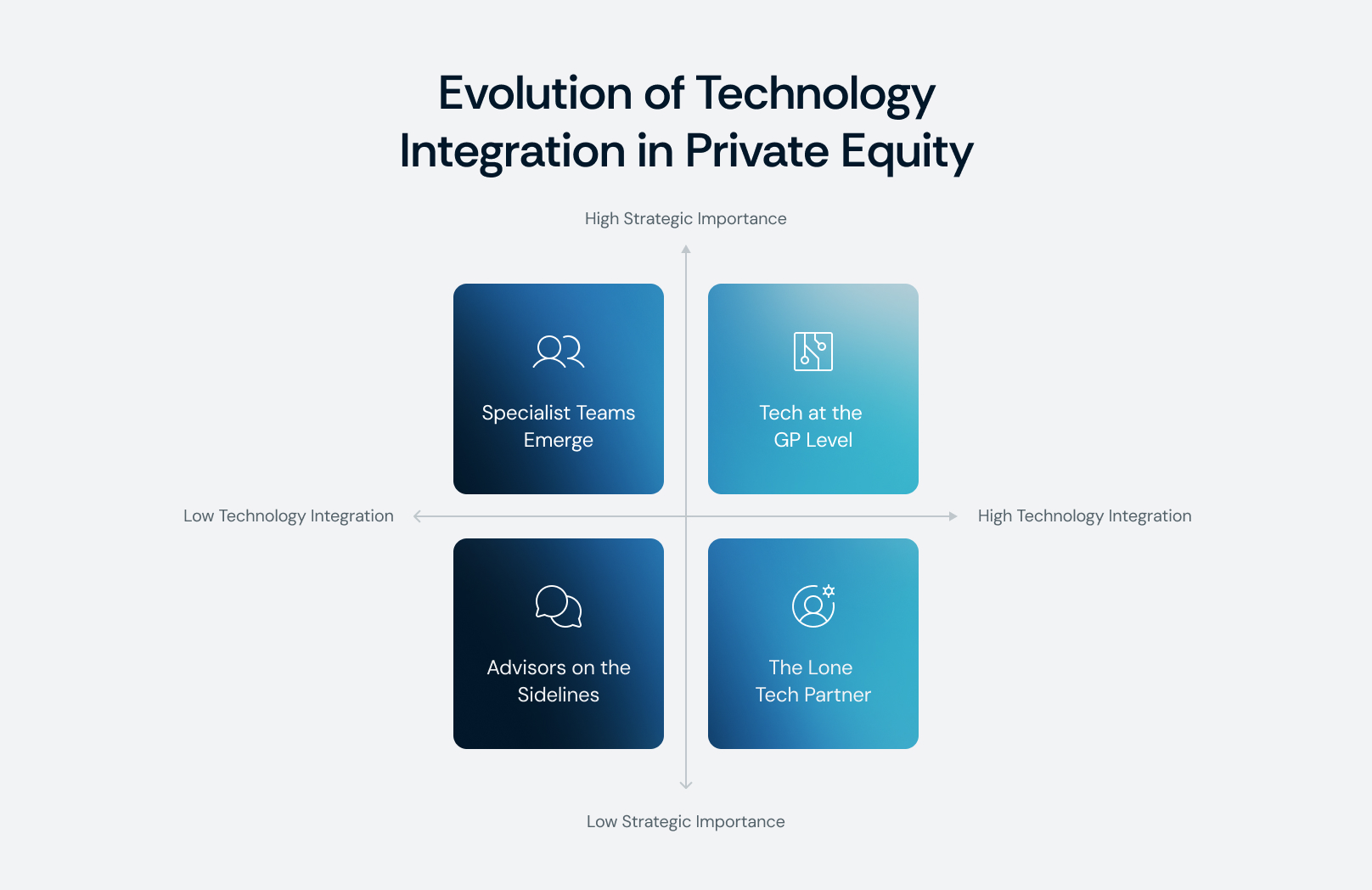

Four Phases of Evolution

- Advisors on the sidelines

Early tech involvement came via external consultants—costly, tactical, and detached. Firms paid for PowerPoints; little changed post-engagement. - The lone tech partner

PE firms began hiring CIOs/CTOs as full-time Technology Operating Partners—“one-person armies” who translated tech for deal teams but lacked bandwidth to scale transformation. - Specialist teams emerge

Firms built full-stack digital teams—AI, data science, cybersecurity, transformation—realizing no one expert could cover it all. Leaders like Apollo and Blackstone now deploy portfolio-wide playbooks through in-house experts and vendor ecosystems. - Tech at the GP level

Today, Technology OPs are embedded in deal teams, attend IC meetings, co-shape investment theses, and hold board seats. Compensation reflects this: $500K–$750K base, $250K–$1M bonus, and carry on par with deal partners (Korn Ferry).

The Emergence of the AI Operating Partner

A new frontier: AI Operating Partners. These roles exploded in 2025, with a 30% spike in demand in Q1 alone(Acertitude). Why? Even veteran tech OPs often lack the depth to architect and implement AI at scale.

Firms now seek rare talent with:

- Hands-on AI experience

- Commercial acumen to identify real use cases

- Leadership ability to drive adoption

Korn Ferry defines three archetypes:

- Entrepreneurial leaders from AI-driven firms

- Product/technical leads with commercial sensibility

- Enterprise IT execs experienced in scaling AI

How Leading Firms Are Structuring for Scale

- Apollo: Vikram Mahidhar leads Data, Digital & AI for 40+ portfolio companies, supported by strategic partners like Figure and Motive.

- Blackstone: Rodney Zemmel, former McKinsey Digital leader, oversees tech across 250 companies alongside CTO John Stecher (Barclays, Goldman, IBM).

- Bain Capital: Hired Jordi Diaz (ex-QuantumBlack, PhD in EE) to lead data science and AI across fund strategies.

- Carlyle: Promoted internal leaders like Georgette Kiser (former CIO) and Board member Sharda Cherwoo (EY’s AI lead).

- Vista: Requires all portcos to submit generative AI goals annually; runs GenAI CEO Councils and global hackathons. Bain estimates Vista’s AI efforts could boost software margins so significantly it rewrites the “Rule of 40” to the Rule of 50–60.

Compensation Confirms the Shift

Heidrick & Struggles data shows rising turnover at tech and IT consulting firms due to intense PE demand. McKinsey/Bain/BCG alumni command 8–11% premiums, and digital transformation talent drives even higher bids.

Why Tech-Native Operating Partners Are Replacing Traditional Executives

The gap between technology-native operating partners and traditional operators isn't just about credentials—it's a wholesale divergence in capabilities, experience, and how value is created.

Deep Technical Foundations

Traditional OPs typically hold MBAs and rose through general management. Tech-native OPs often have PhDs in computer science, engineering, molecular biology, or data science—like Rodney Zemmel (Cambridge), Jordi Diaz (NJIT), and others from MIT, Stanford, and Carnegie Mellon. These backgrounds give them fluency in quantitative methods, system architecture, and AI/ML—skills critical for today’s portfolio needs.

Career Paths That Build Systems, Not Just Teams

Traditional OPs built careers managing across functions. Tech OPs built products. They’ve coded, scaled platforms, led data science teams, and architected systems at Palantir, Microsoft, IBM, and startups. They can assess technical debt, vet CTOs, and gauge real delivery capabilities—not just org charts and KPIs.

Specialized Consulting Experience

Many traditional OPs came from strategy roles at McKinsey, Bain, or BCG. Tech OPs come from McKinsey Digital, QuantumBlack, EY Intelligent Automation, and similar teams—where they led AI, data infrastructure, and transformation initiatives. Their consulting toolkit is designed for execution, not just recommendations.

How They Solve Problems—And Why It Matters

Traditional OPs rely on qualitative diagnostics: interviews, benchmarking, process tweaks. Tech OPs use data instrumentation, analytics, and automation. For example:

- Traditional approach to sales productivity: Restructure territories, revise comp plans.

- Tech-native approach: Use CRM analytics, AI lead scoring, and predictive funnel modeling—often producing 2–3x impact.

Network Value and Execution Oversight

Tech OPs tap deep technical ecosystems: CTOs, AI vendors, engineering leaders. Their connections unlock faster hiring, vendor vetting, and solution deployment. Apollo's partnerships with Figure Technologies and 25madison show how tech OPs scale capability across portfolios.

They also oversee implementation directly—reviewing code, validating architecture, spotting overfitting in AI models, or preempting flawed cloud decisions. Traditional OPs can't catch these execution risks early.

Toolkits That Drive Step-Change Value

Traditional OPs bring incremental playbooks: pricing, procurement, working capital. Tech OPs unlock step-function gains: AI-driven demand forecasting, dynamic pricing engines, intelligent automation of entire workflows.

Risk and Cultural Credibility

Tech OPs quantify risk—data quality, model robustness, cybersecurity, and tech stack sustainability. These risks now drive deal outcomes more than ever.

They also command organizational trust. Engineering and product teams respond better to leaders who “speak their language,” while traditional OPs often get sidelined as non-technical outsiders.

The 5–25% EBITDA Story That Ended the Debate

AI-driven value creation is no longer hypothetical. Across private equity, the numbers are in—5% to 25% EBITDA improvement is now a proven range, not a projection.

Hard Evidence Across the Portfolio

- FTI Consulting (2024): 5–25% EBITDA gains across industries based on live client data, not models. Manufacturing tends to fall on the lower end (predictive maintenance), while sales- and software-heavy businesses hit the top of the range.

- Bain & Company: AI-driven leaders report 10–25% EBITDA improvement, with GenAI initiatives alone potentially adding 20%.

- BCG: Half of surveyed companies expect 10%+ cost savings from AI and GenAI—translating to billions for large enterprises.

Case Studies from the Front Lines

- Apollo’s Portfolio:

- Cengage: 40% content production savings, 15–20% lead generation and software development savings, 15% reduction in customer care costs.

- Cross-portfolio procurement: 65% cost reduction by using AI to review 15,000+ software contracts—value even seasoned procurement teams miss.

- Yahoo: 20%+ engineering productivity gains; 10,000+ AI-generated lines of code accepted daily; enterprise copilots save 1 hour/week/user.

- Barnes Group: 5x ROI in year one from AI-powered technician tools improving first-time fix rates.

- Univar Solutions: 30% reactivation rate from AI-driven outreach to dormant customers.

- Shutterfly: $5M in new revenue and 22% dev productivity boost from AI automation.

- Vista Equity: 30% coding productivity gains portfolio-wide; 80% of portfolio companies now deploying GenAI.

- LogicMonitor: $2M in annual customer savings via AI triage.

- Avalara: 65% increase in sales rep response time with GenAI tools.

High-ROI Functional Areas

- Procurement: 15–45% cost savings. BCG and Efficio cite 8–12% savings on addressable spend; McKinsey reports up to 40% EBITDA gain from optimized procurement.

- Pricing: Highest impact area with 25–50% EBITDA uplift. AI uncovers willingness-to-pay variation, enabling dynamic, optimized pricing by segment and context.

- Sales & Marketing: 15–30% gains from AI-augmented prospecting, conversion optimization, and CAC reduction.

- Software/IT: 10–30% productivity boosts through AI-assisted coding and testing.

- Manufacturing/Ops: 5–25% gains from AI-driven logistics and predictive maintenance.

- Customer Care: 15–40% cost reductions via chatbots, automation, and AI-enabled sentiment analysis.

Speed of Impact

- Fast Paybacks: PwC assessments deliver 25–50%+ EBITDA lift opportunities in just 6–8 weeks. Barnes Group and Shutterfly saw measurable ROI within a year.

- Medium-Term Gains: 12–24 months as companies move from pilots to scaled AI programs.

- Long-Term Compounding: Over 3–5 years, firms build proprietary playbooks and muscle memory—93% of PE firms expect meaningful benefits (World Economic Forum).

The message is clear: AI delivers enterprise-grade, measurable EBITDA uplift faster and more reliably than any traditional lever, making tech-native operating partners indispensable. (World Economic Forum)a

Technology Transformation Equals Procurement Equals Pricing as a Strategic Imperative

The strategic role of technology in private equity has reached parity with traditional levers like procurement and pricing. This marks a structural shift in how PE firms allocate resources, structure operating teams, and prioritize investment strategies.

Operational value creation now drives 79% of PE firms' returns—a stark reversal from decades dominated by financial engineering (Accenture, PwC). EY’s research confirms operational improvements have overtaken multiple expansion as the primary return driver for deals exiting in 2024–2025 (EY).

In 2024, AI and technology became the #1 strategic priority for PE firms, outranking traditional initiatives like working capital optimization and procurement (EY). This reflects not hype but hard ROI—firms now deploy capital and leadership attention where returns are greatest.

LP expectations have followed. 85% of GPs expect AI to significantly reshape operations within five years (EY). LPs increasingly probe for dedicated tech operating partners, in-house data science teams, and proprietary AI tools. Firms unable to answer convincingly face capital reallocation.

70% of GPs expect increased tech deal volume—the highest of any sector. Cost takeout initiatives, long a PE staple, now match tech in priority—not exceed it (EY).

Firms are embedding tech at the highest levels. Digital leaders now report directly to the CEO, not operations. Blackstone’s appointment of Rodney Zemmel—ex-Global Head of McKinsey Digital—as Operating Group Head underscores this (Blackstone).

Technology now spans the full deal lifecycle, from diligence to exit. 80% of firms with $10B+ AUM conduct value creation planning pre-investment, with technology assessments now standard (Moonfare, EY).

Technology’s ROI vs. Traditional Levers

- Procurement: Delivers 8–12% cost savings, representing up to 40% EBITDA growth for midsize firms (Accenture, McKinsey, Efficio).

- Pricing: Generates 3–7% margin expansion, though underutilized due to complexity (McKinsey).

- Technology/AI:

- 10–45% sales growth potential for CPGs (EY)

- Valuation uplifts up to 23% within 12–18 months (AlixPartners, Moonfare)

- 20% distressed inventory reduction via autonomous supply chain tools (EY)

Firms now cite cost, cash, tech, talent, and ESG as the five pillars of value creation (EY). Technology is no longer support—it’s central.

Sector and Capital Allocation Trends

- IT and healthcare nearly doubled their share of PE allocations from 2000 to 2021, driven by digital health and tech-enabled business models (Cambridge Associates).

- Global PE deal value rose from $1.3T in 2023 to $1.7T in 2024, with tech M&A as a key driver. Healthcare tech M&A hit $115B in 2024—second-highest on record (Medium).

- Nearly 40% of McKinsey consulting projects are now AI-related, underscoring tech’s centrality to PE portfolio strategies.

Technology-Infused Traditional Improvements

- Working capital now includes optimizing IT org structures and evaluating tech lease vs. buy options (EY).

- Focus has shifted from reducing tech spend to maximizing ROI from it—recognizing technology as a growth driver, not just a cost center.

Amplifying Traditional Levers Through Tech

- Procurement: 84% of PE leaders prioritize it, now increasingly using AI to enhance results (BCG). Apollo achieved 65% cost reduction using AI to analyze 15,000+ contracts (MIT Sloan Management Review).

A Calculated Bet on Technology

Firms are rational capital allocators. That they now prioritize technology reflects measured confidence in ROI. Companies implementing digital transformation see 23% higher valuations on average (Moonfare).

McKinsey’s 2025 report confirms the pivot: “Dealmakers and operators are moving from traditional financial engineering to sustained operational transformation”—with technology at the center.

And as Cambridge Associates states: “PE managers no longer seem to be cutting their way to value.” Instead, they’re using AI, data science, and digital tools to drive top-line growth and sustainable margin expansion. The playbook has changed—and technology is now page one.

The Organizational Models That Separate Winners from Pretenders

The real divide in PE today lies in how firms build and embed technology capabilities—not in rhetoric, but in structure, scale, and cultural integration.

Scale and Depth Matter

Top-performing firms don’t stop at one or two tech‑oriented hires. They build teams of 10–30 deep experts across AI, data, transformation, cybersecurity, and cloud. Apollo’s Data & Digital Transformation team spans 40+ portfolio companies under Vikram Mahidhar’s leadership. Blackstone coordinates data science and AI transformation across 250+ companies. (See how Rodney Zemmel heads its operating group.) [Blackstone] Bain Capital even created a Managing Director role dedicated to firm‑wide AI and data strategy.

Placement Signals Priority

When tech OPs are elevated to General Partner status or report directly into the GP group, technology is clearly not an afterthought. That’s what Blackstone did by naming Zemmel to lead all operating functions—not just tech. In contrast, firms that tuck tech under COOs or silo it within operations signal superficial commitment.

Embedded From Day Zero

Winners integrate technology into origination, diligence, and investment committees, not just post-close. They send tech OPs on pre-LOI diligence to assess stacks, data architecture, security posture, and transformation needs. They show ICs granular tech roadmaps, investment needs, risks, and EBITDA upside. That’s vastly different from firms where tech OPs only see the portfolio after closing—by which time the 100-day agenda window has passed.

Proprietary Partnerships and Tools as Moats

Genuine winners cultivate proprietary tech ecosystems. Apollo partners with Figure, Motive, and its own incubator (25madison) to bring next-gen capabilities into the fold—not as external vendors, but as internal resources. Vista’s AI-first planning, hackathons, and GenAI Council push shared innovation across its portfolio. These moats can’t be bought overnight.

Data Aggregation = Information Advantage

Advanced firms build cross-portfolio benchmarks. Apollo’s procurement AI analyzes thousands of contracts using firm-wide data, surfacing cost savings invisible at the company level. The result: newly acquired companies jump several quarters ahead on improvements.

Talent Density and Credibility

The difference is in who's doing the work. In high-performing firms, tech OPs have PhDs, built AI product at tech companies, and lead communities of engineers and data scientists. In contrast, firms hiring former CIOs from legacy enterprises often lack the domain fluency needed to evaluate tradeoffs, APIs, ML models, vendor roadmaps, or infra scale.

Four AI Operating Models (FTI’s Framework)

FTI identifies four models of AI deployment maturity:

- Fully Decentralized – Portcos manage AI independently—slow, fragmented learnings

- Center-of-Excellence – Shared knowledge but limited central execution

- Fund-Level Model – Central AI team serves portfolio-wide but doesn’t enforce standardization

- Centralized AI Operating Model – Fully centralized AI team powerhouses execution across all funds

The last model maximizes scale, consistency, and learning.

Resource Commitment as a Proof Point

Allocations matter. PE firms investing $50M+ in AI (just ~0.25% of a $20B fund) are 1.3x more likely to capture cost savings than those investing less. Spending small suggests theater. Committing capital says “this is central to our playbook.”

Organizational Change > Technology Tools

Successful AI transformations are less about algorithms and more about mindset. Only about 20% of transformation success comes from tech; 80% from change management, culture, and process alignment. Firms that treat tech as a plug-in tool fail. Firms that treat it as organizational DNA win.

Measurement, Incentives, and Attribution

Best-in-class firms benchmark digital maturity at acquisition, track progress quarterly, and credit EBITDA gains to tech initiatives transparently. They intervene early when projects stall. They tie compensation and carry to tech performance. That level of rigor propels growth.

Recruiting Distinguishes Builders from Pretenders

Firms that hire AI/tech leaders from McKinsey Digital, QuantumBlack, top tech firms, or AI startups show real intent. Those hiring generic “digital transformation consultants” or ex-IT executives from legacy industries are often just checking box for LPs. And in this war, compensation and carry must compete at PE levels to attract top talent.

What Limited Partners Now Demand — And Why It Matters

In just three years, LP due diligence on tech capabilities shifted from optional to mandatory. Today, technology operating partner excellence is frequently a binary filter: funds without it risk allocation cuts or exclusion, regardless of their track records.

The Reset in LP Priorities

LPs learned tough lessons from 2020–2024:

- Funds raised in the zero‑rate era have struggled—multiple expansion reversed, leverage costs surged, and portfolios without operational muscle failed to grow.

- Distributions dropped to 14.6% of NAV in 2022; Q1 2023 saw distributions of just 2.2%.

- Unrealized value swelled 131% between 2019 and 2023, from $1.1T to $2.5T.

These trends convinced LPs that financial engineering alone is no longer sufficient.

What LPs Now Ask

During fundraising, LPs probe to distinguish substance from show:

- How many dedicated tech OPs do you have?

- What are their credentials—do they have hands-on AI/data experience?

- Do they sit on the investment committee and influence deal selection?

- What % of deals undergo technology due diligence pre‑LOI?

- Can you quantify EBITDA impact of past tech initiatives?

- Is tech OP compensation tied to carry or fund performance?

LPs expect answers that reflect scale and substance—not token hires or half-measures.

How LPs Judge Returns

It’s not just about returns—it’s about how they were achieved. LPs now analyze exits to see whether value came from tech-enabled growth and margin expansion or merely market multiples. They know that returns relying on market tailwinds are fragile; the signals of enduring value lie in operational execution.

The Capital Redistribution Game

Top-tier funds increasingly capture disproportionate capital. In 2024, six firms captured ~60% of the fundraising—a steep rise from 20% in 2019. The reason: they built technology platforms over years. Blackstone supports 250 portfolio companies; KKR’s Capstone has 100+ operating chiefs globally; Apollo built a Data & Digital Transformation arm. LPs back what they see is scalable, capability-based edge.

What Smaller and Mid-Market Firms Face

The question is existential: how to compete when tech talent flees to established platforms? Some pursue specialization (e.g. software-only or industry tech edges), others partner with consultancies or vendors. Some accept that tech sophistication is a gap and reposition to sub-sectors where tech is less central. But the window is narrowing fast.

Messaging Has Changed

Tech now dominates LP pitch decks. GPs lead with technology OPs, show proprietary AI tooling, quantify tech‑driven EBITDA, and integrate tech into investment theses from screening through exit.

More Than a Trend—Survival Stakes

Fundraising is harder: median time to close rose from 11.2 months to 18.1 months in two years. First-time funds struggle. LPs increasingly lean into proven operational capability as the gatekeeper for capital deployment.

LP Strategic Concerns

- Overpay risk — Without tech fluency, GPs may misjudge remediation costs or hidden technical liabilities.

- Competition risk — Companies now compete on tech. A PE owner lacking operational tech support may handcuff management.

- Exit discounts — Buyers penalize legacy systems and tech debt. Without tech credibility, GPs lose value at exit.

- Talent attraction asymmetry — CEOs and executives gravitate toward sponsors who can add tech value. GPs without tech platforms face adverse selection.

The Path Forward — And What It Requires

Private equity firms face a binary choice: build institutional technology capabilities that drive systematic value creation across portfolios, or accept permanent competitive disadvantage. The window for catching up narrows quarterly as leading firms compound their advantages through proprietary tools, accumulated knowledge, and network effects.

1. Executive Commitment & Resource Allocation

Change must start at the top. Founding partners and senior leadership must champion technology operating capabilities, explicitly positioning technology as co-equal with traditional value creation levers. This means allocating meaningful percentages of management fees—typically 5–10% for mega-funds, 10–15% for mid-market firms—to build and maintain technology operating teams. The investment feels expensive until compared to returns generated: if technology focus adds 2–3 percentage points to IRR at 3x MOIC, a $5 billion fund generates $300–450 million in additional value against perhaps $200–250 million in operating costs over fund life.

2. Talent Strategy for Tech-First Capabilities

The recruiting must be targeted: senior partners from McKinsey Digital, QuantumBlack, former CTOs, Chief Data Officers, engineering leaders from technology firms, or AI specialists from companies like Palantir or Google DeepMind. Former technology executives from PE portfolio companies bring domain fluency plus operational depth.

3. Genuinely Competitive Compensation

Compensation must reflect the strategic value of technology. Senior tech OPs now receive base salaries of $500K–$750K, bonuses of $250K–$1M, and carry allocations of 1–3% individually or 10–20% collectively (Heidrick & Struggles). Undercompensated teams will lose talent to tech firms or competitors.

4. Integration in Deal Flow

Technology OPs should have full participation in investment committees, conduct diligence pre-LOI, and shape investment theses with clear digital strategies. Some firms—like Blackstone—have promoted digital leaders like Rodney Zemmel to lead entire operating teams, signaling equal weight between investment and operational expertise.

5. Embedded Post-Close Engagement

Tech OPs should lead during the first 100 days, conducting digital readiness assessments, developing transformation roadmaps, and identifying tech gaps. Ongoing involvement ensures progress tracking and avoids transformation stall-outs.

6. Tooling & Systems Investment

Firms must invest in benchmarking systems, playbook repositories, AI-assisted operating tools, and dashboards tracking KPIs portfolio-wide. Firms like Apollo aggregate procurement and digital maturity data across 40+ companies to find hidden optimization opportunities (MIT Sloan Management Review).

7. Vendor & Talent Ecosystems

Proprietary partnerships—like Apollo's work with Figure Technologies, Motive Partners, and 25madison—create sustained tech edge. Building academic and talent networks early compounds hiring and sourcing advantages.

8. Knowledge Management

Tech OPs should document successful projects, quantify impact, and build repeatable templates for implementation. Forums like Vista’s GenAI CEO Council facilitate best-practice exchange across portfolios.

9. Quantitative Attribution & Accountability

Firms must rigorously measure technology contributions using dashboards and attribution models. LPs increasingly demand visibility into specific AI-enabled EBITDA improvements and want to know how tech OPs are compensated and involved.

10. Initial Scale Strategy for Emerging Firms

Firms catching up should start with a few exceptional hires empowered as equals—not subordinated to deal teams—and place them immediately into diligence and 2–3 live transformations. Case studies generated in year one provide credibility with LPs and internal advocates.

11. Hybrid Team Structures

Smaller firms can combine 1–2 full-time tech OPs with a broader expert network, offering flexible compensation like success fees, equity, or co-investment options.

12. Build Time: 24–36 Months

Institutional capabilities don’t materialize overnight. Plan for:

- 0–9 months: Hire and pilot

- 9–24 months: Scale playbooks, build infrastructure

- 24–36 months: Embed fully into fund strategy, diligence, and exits

13. The Risk of Inaction

Firms lacking these capabilities are already paying the price—through missed risks in diligence, lost deals, portfolio underperformance, and LP reallocations. Accenture, EY, and McKinsey all now show operational tech excellence as the core driver of returns.

Conclusion: The Permanent Reconfiguration of Value Creation

The shift from traditional operator profiles to technology‑first, AI‑native operating partners marks PE’s most consequential capability transformation in decades. This isn’t a cyclical trend—it’s a structural realignment in how companies compete and value is created. The firms who bet early on tech ops now compound that advantage across fund cycles.

The data leaves no room for doubt. Experts document 5–25% EBITDA gains from AI and digital transformation across industries—returns that rival or exceed procurement or pricing improvements. And while traditional levers are largely tapped out in many portfolios, the runway for technology and AI remains expansive.

The moves made by leading firms make the stakes visible. Blackstone’s appointment of Rodney Zemmel (former McKinsey Digital head) to lead their entire operations signals operations and technology are now inseparable. Blackstone

Apollo’s Data & Digital Transformation team, spanning 40-plus portfolio companies and backed by proprietary tools and partnerships, shows tech needs institutional infrastructure. MIT Sloan Management Review+2Apollo+2

Bain Capital’s decision to create a Managing Director for AI/data strategy underscores the necessity of elevating these capabilities to the C‑suite. (Internal example.)

Talent dynamics reinforce permanence. Requests for AI Operating Partner roles jumped 30% in Q1 2025, and AI-focused skills rank among the top five most demanded for operating teams. Compensation now approaches investment partner levels—including $500K‑$750K base, $250K‑$1M bonuses, and meaningful carry participation.

Limited partners have shifted their bar entirely. During fundraising, they now rigorously evaluate tech OP credentials, demand quantification of EBITDA from tech initiatives, and expect tech teams to influence deal selection and valuation. Weak answers lead to delayed closes or reduced allocations.

Competitive spirals amplify advantages. Firms with strong tech platforms win more deals, outperform operationally, raise capital more efficiently, and reinvest aggressively. Those without fall further behind.

The window for building competitive tech operating capabilities still exists—but it’s narrowing. Over a 24–36 month horizon, firms can move from nascent efforts to fully integrated tech operations—but only with urgent clarity, resources, and leadership discipline. For funds of typical scale, a 2–3 point IRR lift from tech yields hundreds of millions in incremental value—more than enough to justify the $25–50 million per year often required for a world-class tech ops team.

Crucially, technology must be institutionalized—not superficial. Success demands recruiting PhDs, AI operators, tech OPs from peer firms, paying top-tier packages with carry, and integrating tech deeply into deal and portfolio management.

For leaders today, this is more than a strategic move. It’s a reset: technology has earned permanent parity with procurement, pricing, and operations. The firms that operate with that belief—they structure for it, fund it, and lead it—are writing the blueprints for the next generation. Those who resist or delay will struggle until the gap becomes insurmountable.

Private equity is reengineering how value gets made. The new operating partner has to be a technologist first. And the winners are already building that future.