The Diligence Integration Imperative: Why Operating Partners Hired After Deal Close Arrive Too Late

- Firms integrating operating partners from diligence through exit generate 3.8–4.5% higher IRRs and hundreds of millions in added value compared to post-close engagement.

- Market realities—11x EBITDA entry multiples, 4–5% interest rates, 5–7 year holds, and LP distribution pressure—make early operational integration essential, not optional.

- 62% of firms still wait until post-close, clinging to outdated models built for financial engineering.

- The choice is binary: embed operating partners from diligence onward or accept permanent competitive disadvantage.

- Leading firms are already institutionalizing early integration with IC processes, carry alignment, and day-one 100-day plans.

- Firms delaying will lose deals, LP capital, and eventually relevance—the gap is widening into organizational survival versus obsolescence.

Private equity firms that wait until after close to bring in operating partners are systematically destroying value. The evidence is clear: funds that integrate operational due diligence alongside financial DD and build detailed value creation plans pre-LOI achieve IRRs 3.8–4.5 percentage points higher than peers. On a $2 billion fund, that gap translates into $150–250 million in additional value—the difference between top-quartile performance and mediocrity. Yet 62% of firms still treat operations as a post-acquisition exercise rather than a core diligence function.

In today’s market, that mistake is existential. With median purchase multiples at 11.2x EBITDA—nearly double the 2010–2015 average—returns hinge on flawless execution. The margin for error has disappeared. Firms that uncover operational gaps three months after closing have already wasted the critical first 100 days, when management is most receptive and transformation gains the most traction.

The problem isn’t talent—it’s process. Many firms employ world-class operators with deep functional expertise, but sideline them until the ink is dry. Deal teams develop theses, run diligence, and negotiate terms without operational input. Only after capital is deployed do they introduce operating partners, hand them a consultant-built “value creation plan,” and expect immediate impact. By then, the opportunity has already decayed.

This article explores why post-close involvement destroys value, how leading firms embed operating partners throughout the deal lifecycle, what true pre-LOI operational diligence looks like, and the quantifiable performance gap between firms that get this right and those that don’t. The conclusion is blunt: separating deal-making from operations is no longer just outdated—it’s financially catastrophic. Firms embedding operators from initial screening through exit are pulling decisively ahead. Those sticking to traditional handoffs face permanent disadvantage.

The Catastrophic Cost of Post-Close Operating Partner Engagement

The traditional PE playbook is sequential: deal teams source, diligence, negotiate, close—and only then bring in operating partners to drive value creation. That model worked when financial engineering and multiple expansion drove returns. In 2025, with operational improvements contributing 47% of PE value creation and multiples compressing, it’s a recipe for failure.

The data is conclusive. Analysis of 1,200+ deals shows firms involving operating partners pre-LOI deliver median IRRs of 18.7% versus 14.2% for post-close engagement—a 4.5 point spread worth $150–$250 million on a $2B fund. Bain finds companies with 100-day plans built during diligence achieve 2.1x higher year-one EBITDA growth. BCG reports early operating involvement cuts CEO turnover by 34% and CFO turnover by 41%. The gap compounds over holding periods.

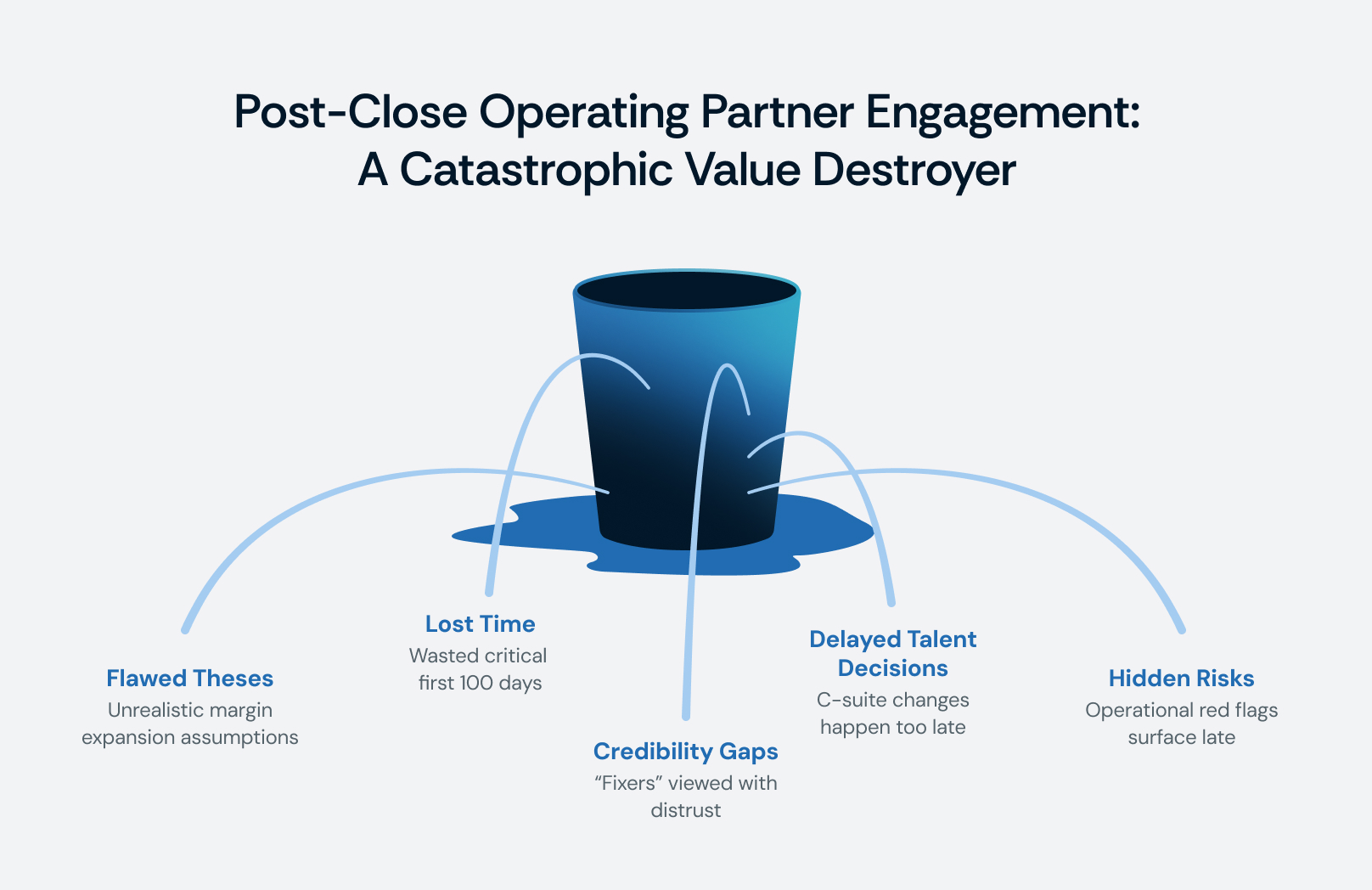

Why? Post-close engagement sets off cascading failures:

- Flawed theses — Deal teams without operational depth underwrite 500bps of margin expansion or double-digit growth without validating whether systems, talent, or processes can deliver.

- Lost time — The first 100 days—the transformation “honeymoon”—are wasted on orientation, not execution. By the time operating partners act, urgency has evaporated.

- Thesis vs. reality — Operating partners often find that pricing, product mix, or cost targets assumed in diligence are unrealistic, but the deal is already closed at those valuations.

- Credibility gaps — Management sees operating partners as “fixers” parachuting in late, not trusted partners who shaped the thesis pre-deal. Trust erodes before work begins.

- Delayed talent decisions — 73% of successful PE transformations involve C-suite changes within six months. Post-close engagement pushes these decisions to month 9–15, too late to capture first-year value.

- Hidden risks — From broken tech stacks to overstated working capital, operational red flags surface only after capital is committed—forcing operating partners to quietly absorb problems rather than reset strategy.

The opportunity costs are measurable: companies with early operating involvement capture 65% of targeted margin improvements in year one versus 38% post-close; $4.7M in average cash liberation versus $1.9M; 84% of revenue targets hit versus 61%. CEO turnover nearly doubles (47% vs. 22%), costing portfolios $12–20M in direct expenses plus 12–18 months of execution delay. M&A integration succeeds 78% of the time with pre-deal operating diligence, but only 43% post-close.

The math is brutal: missing year-one targets because operating partners arrived late often means never making them up before exit pressure forces a sale. In today’s market, separating deal-making from operations isn’t just outdated—it’s financially catastrophic.

What Pre-LOI Operational Due Diligence Actually Entails

Leading firms now embed operating partners into diligence from the moment a target is seriously pursued—well before LOI. This isn’t box-checking; it’s a 3–5 week, multi-dimensional analysis that determines whether the investment thesis is operationally achievable.

The process begins at IOI or preliminary diligence. Deal teams brief operating partners on the thesis and preliminary financials, and operators immediately frame hypotheses about value creation opportunities and risks. From there, the work becomes granular and systematic:

- Management meetings (weeks before LOI): While deal partners focus on strategy and numbers, operating partners conduct structured interviews with the CEO, CFO, COO, and key leaders, probing operational depth rather than surface-level narratives.

- Commercial operations: Assessment covers pricing sophistication, sales productivity versus benchmarks, customer concentration and retention, contribution margins by product/service, marketing ROI, and the quality of CRM and enablement tools. The question isn’t whether growth is possible—it’s whether the company has the systems to execute.

- Operational infrastructure: For manufacturers, this means analyzing OEE, maintenance regimes, and production planning. For service businesses, it’s workflows, utilization, project management, and quality control. The goal is to separate process-driven maturity from reliance on “tribal knowledge.”

- Financial operations: FP&A rigor, forecasting accuracy, working capital discipline, accounting controls, and reporting speed all get scrutinized. Weak finance infrastructure stalls execution post-close; firms with early insight can price remediation into the deal.

- Technology stack: Operators evaluate ERP maturity, BI and analytics capabilities, cybersecurity posture, digital channels, and IT leadership. Legacy systems or technical debt can add tens of millions in hidden costs—critical to know before signing an LOI.

- Talent and leadership: With 70%+ of PE-backed companies replacing CEOs during ownership, pre-close leadership assessment is essential. Operators evaluate the CEO’s scalability, stamina, and cultural fit, identify weaknesses in the C-suite and bench, and assess change-readiness. If a CEO needs replacing, firms can plan transitions before committing capital—not nine months after close.

- Specific initiatives, not abstractions: Operating diligence translates into quantified roadmaps, e.g.:

“3% price lift on bottom 40% of customers adds $4.2M EBITDA. Requires 9 months of CRM upgrades, $600K capex, with attrition risk limited to $3M revenue across 8–10 accounts.”

Replicate that level of specificity across 15–25 initiatives, and a generic thesis becomes an actionable plan.

All findings feed directly into investment committee and LOI structuring:

- IC memos include an operational capabilities section authored by operating partners.

- LOI terms incorporate identified risks—ERP replacement costs, CFO transitions, customer concentration earn-outs, or key talent retention packages.

The time commitment is significant: 60–100 hours per deal, spanning interviews, site visits, data analysis, and roadmap development. But for deals priced at 11x+ EBITDA, this diligence is no longer optional—it’s the difference between confident underwriting and expensive surprises.

100-Day Plans Developed During Diligence, Not Post-Close

The 100-day plan is private equity’s most critical operational tool—yet most firms build it at the wrong time. Developing plans post-close wastes the first 100 days, the period when momentum and management receptivity are highest. Leading firms now build detailed, execution-ready 100-day plans during diligence, aligning them with the investment thesis and ensuring day-one readiness.

A robust 100-day plan is typically 30–50 pages and covers:

- Week-by-week milestones across the first 100 days.

- Top 3–5 operational initiatives with owners, budgets, and timelines.

- Key talent decisions, including C-suite changes and critical hires.

- Infrastructure projects, such as ERP upgrades or process redesigns.

- Governance structures, with cadence for metrics reviews, board meetings, and reporting.

The cadence matters:

- Days 1–30: Quick wins. Establish trust, launch fast-impact initiatives (procurement renegotiations, targeted price increases, working capital improvements).

- Days 31–60: Major initiatives. Launch core projects like pricing analytics, ERP migrations, or salesforce redesigns.

- Days 61–90: Scaling. Expand pilots into full deployments and institutionalize new disciplines.

- Days 91–100: Transition. Assess progress, course-correct, and define the 6–12 month roadmap.

Specificity is the difference-maker.

- Generic post-close plan: “Improve gross margins by 300 bps through pricing optimization. Target $4.5M EBITDA in 12 months.”

- Diligence-developed plan: “Implement value-based pricing for professional services (40% of revenue, currently priced 12% below market). Deploy analytics tool ($125K, Days 15–45), raise prices 8% for bottom-quartile customers ($1.8M EBITDA uplift net of churn risk, Days 46–75), restructure bundles with sales training ($75K, Days 60–90). Net EBITDA impact: $2.1M in Year One.”

With pre-close planning, analytics tools are procured, segmentation analysis is already underway, and leaders are briefed before the deal closes—allowing execution to start on Day 1, not Day 60.

Governance clarity is another advantage. Effective diligence-developed plans specify reporting cadences (weekly metrics reviews shifting to bi-weekly), board schedules (monthly early on, then quarterly), and leading KPIs tailored to the thesis (e.g., pipeline growth, OEE, defect rates) rather than lagging indicators.

Talent moves also get de-risked. If the CFO must be replaced within 60 days, the plan specifies search strategy, interim options, and rollover adjustments before closing—not months later when value has already leaked.

The investment required is modest relative to the upside: 30–50 hours of operating partner time, often supplemented by $50K–$100K for targeted expert validation. Yet the payoffs are significant: companies with pre-close 100-day plans achieve 87% of day-100 milestones (versus 34% post-close), launch initiatives 47 days faster, generate $3.8M more EBITDA in Year One, and reduce C-suite turnover by a third. Across a 10-company portfolio, that equates to $20–35M in added value for just 400–600 hours of work.

How Top Firms Integrate Operating Partners Throughout the Deal Lifecycle

The firms that consistently deliver outperformance—KKR, Bain Capital, Vista, TPG—treat operating partners as central to the investment process, not as post-close problem solvers. Their models embed operating perspectives from deal sourcing through exit, backed by governance, compensation, and culture that give operators equal footing with dealmakers.

1. Early Screening

Operating partners participate in weekly or bi-weekly pipeline reviews. They flag operational red flags (unsustainably low margins, customer concentration, technical debt) and pressure-test whether realistic value creation levers exist. This filters out deals that lack viable operational theses before resources are wasted.

2. Pre-LOI Diligence

When a target advances, a designated operating partner becomes the deal’s operational lead. They run parallel diligence alongside financial and legal work: structured interviews with management, operational maturity assessments, talent evaluations, and early 100-day planning. Findings directly inform IC materials, LOI terms, and valuation—ensuring operational feasibility is vetted before capital is committed.

3. Investment Committee

At top firms, operating partners present directly to IC or sit alongside deal partners to answer questions. Materials include sections authored by operating teams on value creation initiatives, talent risks, and execution roadmaps. Some firms even grant operators effective veto power: if the operational thesis doesn’t hold, the deal doesn’t get approved.

4. LOI-to-Close Integration

Operating partners shape transaction terms—adjusting for required tech upgrades, retention packages, or earn-out structures tied to integration milestones. They also join management meetings to build credibility and socialize the 100-day plan before close.

5. Post-Close Execution

On day one, operating partners are ready to act, not orient. They spend significant time on-site in the first 90 days—often 40–60%—launching quick wins, establishing reporting cadences, and cementing credibility with management.

6. Ongoing Portfolio Management

Operating partners serve on boards, maintain direct ties to CEOs and functional leaders, and lead cross-portfolio initiatives like procurement programs or ERP upgrades. Their portfolio-wide view allows them to spot patterns, deploy shared resources, and accelerate talent placement far faster than deal teams alone.

7. Exit Preparation

Six to 12 months before exit, operating partners professionalize reporting, close operational gaps, and prepare materials highlighting value created. They often join buyer meetings and due diligence, credibly articulating why improvements are sustainable. Their involvement not only strengthens valuations but also builds trust with management teams who care about the company’s next owner.

8. Governance & Culture

The integration works only because firms give operating partners true authority: board seats, IC participation, and carry allocations comparable to deal partners. Team capacity is managed—about 0.75–1.25 operators per investment professional—to ensure depth. Most importantly, culture reinforces that operations drive returns; at leading firms, operating partners rise into firm leadership, not remain siloed.

The result is a fully integrated model where operational insight shapes every deal decision, creating consistent, compounding advantages in both returns and reputation.

The Quantified Performance Gap Between Early and Late Operational Involvement

The evidence is overwhelming: private equity firms that integrate operating partners from the very start of diligence consistently deliver superior returns. Multiple independent studies, across thousands of transactions, converge on the same conclusion—timing is everything.

A joint Oliver Wyman–Wharton study of 1,847 buyouts (2015–2022) found that early integration (operating partners engaged at IOI stage) produced median IRRs of 21.4%, compared to 16.9% for moderate integration (post-LOI) and just 13.6% for late integration (post-close). The MOIC spread was equally stark: 3.2x vs. 2.1x. On a typical $150M equity check, that’s a $165M swing in value—compounded across a portfolio, billions in lost upside.

McKinsey research on 600 mid-market deals reinforced the picture. Companies with pre-LOI operational due diligence achieved 53% higher EBITDA growth (14.8% CAGR vs. 9.7%). Working capital efficiency improved 2.4 percentage points more, freeing up millions in cash, while customer retention rates were 4 points higher.

Execution speed tells the same story. Firms with early integration launched first initiatives in 22 days on average, compared to 87 days for late integration. Within the first year, early-integration companies completed 68% of plan initiatives versus 41% for late starters. Bain’s 2024 analysis showed that diligence-driven 100-day plans enabled companies to hit 73% of first-year EBITDA targets, versus 49% for those built post-close.

Talent decisions amplify the gap. Bain found that CEO changes within six months (possible only with pre-close assessments) delivered 2.8x MOIC, compared to 2.1x for later replacements. CFO transitions followed the same pattern, with early moves tied to 18% higher EBITDA growth.

BCG’s sector-specific research showed that identifying technology debt during diligence boosted IRRs by 4.2 points—since remediation costs were priced in, timelines planned, and crises avoided. Harvard research confirmed longer CEO tenure (4.2 years vs. 2.5) when operational DD included leadership assessments, reducing costly churn.

The advantage only grows in tough markets. University of Chicago analysis found early integration added 5.1 IRR points in downturn vintages versus 2.4 in strong markets—proof that operational rigor provides downside protection when financial engineering fails.

LPs see it too. Preqin’s 2024 survey of 350 LPs ranked “early operational integration” as the second-most important driver of GP outperformance—ahead of deal sourcing.

Across fund sizes, the pattern holds: mega-funds capture +2 IRR points, lower mid-market funds +3.2, and mid-market funds +4.5—the largest differential, since mid-market companies combine scale with operational headroom.

The capital efficiency math is staggering. For a $2B fund making 12 investments, early integration creates $1.2B more value than late integration. For GPs, that translates into $240M of incremental carry. Against operating partner costs of $500K–750K per deal, the ROI is 300:1.

The conclusion is unmistakable: firms delaying operating partner involvement until post-close are not just leaving money on the table—they are structurally underperforming. In a market where operational improvements drive nearly half of all value creation, early integration has become the line dividing top-quartile funds from mediocrity.

Organizational Barriers—and How to Overcome Them

If early operating partner integration produces such clear returns, why do 62% of firms still default to post-close engagement? The answer isn’t technical—it’s cultural, political, and structural.

The biggest barrier is deal team ownership psychology. Most firms operate on a model where deal partners “own” transactions from sourcing to exit, with reputation and compensation tied directly to outcomes. Bringing in operating partners pre-LOI feels threatening: they might slow down deals, raise inconvenient truths, or dilute credit for success. This zero-sum mindset—seeing operations as subtractive rather than additive—undercuts collaboration.

Compensation structure magnifies the tension. When deal partners receive 5–15% of carry while operating partners hold just 0.75–2%, every hour of operating engagement looks like cost, not investment. A $100K+ allocation of operating partner time feels like dilution, even if fund-level returns increase.

Organizational design reinforces this imbalance. At many firms, operating teams report into deal groups, lack partner titles, and have no voice on the investment committee. This subordination signals that operations “advise but don’t decide,” making early integration look like overhead rather than a core diligence function.

The success trap creates another hurdle. Partners who thrived during the 2010s—when entry multiples averaged 7x and leverage drove half of value creation—see little reason to change. Suggesting early operational integration feels like questioning their legacy. They underestimate how radically the environment has shifted: at today’s 11x entry multiples and 5% interest rates, operational execution is no longer optional.

IC dynamics add resistance. Investment committees are often dominated by deal partners. When operating partners raise concerns about execution feasibility, they risk being branded “deal killers.” In cultures where ICs rubber-stamp most presented deals, operational objections feel disruptive rather than protective.

Capacity constraints also matter. A two-person operating team simply can’t cover 10+ live deals in diligence while supporting an existing portfolio. The choice becomes: spread too thin, delay processes, or hire more operators. Many firms punt, leaving operating input shallow or inconsistent.

Finally, knowledge gaps play a role. Deal partners excel at financial modeling but often lack operational fluency; operating partners understand transformation but may not know deal structuring pressures. Without mutual training, conversations stall and mistrust builds.

Overcoming these barriers requires deliberate organizational change:

- Top-down commitment. Senior leadership must make early integration non-negotiable, backed by metrics (e.g., % of deals with operating input pre-LOI) and governance (IC memos with mandatory operating sections).

- Governance redesign. Operating partners should co-own IC materials, present directly to committees, and have veto or soft-block authority when operational theses don’t hold.

- Capacity planning. Realistically, one senior operator can engage deeply in 6–10 deals per year. Firms must staff accordingly, often doubling operating headcount over 12–18 months.

- Carry alignment. Shifting 10–15% of fund carry to operations reframes integration as growing the pie, not slicing it thinner. Deal partners get a smaller share of a much larger outcome.

- Cultural transformation. Celebrate operational wins as loudly as deal closes, promote operators to firm leadership, and feature them prominently in LP materials.

Change doesn’t happen overnight. It typically takes 18–36 months to move from token engagement to institutionalized integration. The path runs through pilots, scaled hiring, governance reform, and cultural reinforcement. Firms that commit see IRR gains of 3–5 points; those that hesitate remain trapped in outdated models.

The Imperative Moving Forward

Private equity has reached a defining moment in how it approaches operational value creation. The evidence is conclusive: firms integrating operating partners from initial diligence through exit generate IRRs 3.8–4.5 percentage points higher than peers that engage operations post-close, with MOIC multiples 0.6–1.1x higher and meaningfully stronger execution across operational metrics. On typical fund sizes, these differences compound into hundreds of millions in additional value—the line between top-quartile performance and mediocrity.

Market conditions have made early operational integration essential, not optional. With purchase price multiples averaging 11x EBITDA, there is no slack for missed execution. Interest rates at 4–5% have stripped away leverage as a return driver. Holding periods of 5–7 years require sustained transformation, not opportunistic timing. And LPs, facing shortfalls in distributions, now demand tangible operational impact—not just promises.

Yet 62% of firms still engage operating partners primarily after close, clinging to organizational models built for a financial engineering era. These firms face a binary choice: redesign their investment process to embed operating partners from diligence onward, or accept permanent competitive disadvantage. The barriers—deal team autonomy, compensation structures, cultural inertia, bandwidth constraints—are real but surmountable. What’s required is leadership willing to treat operational integration as a strategic imperative, invest in the talent and tools, and confront legacy practices that no longer work.

For firms choosing to compete on operational excellence, the path forward is clear. Build sufficient operating partner capacity to engage in every material deal. Restructure IC processes so no LOI proceeds without operational input. Align incentives by giving operating partners meaningful carry tied to fund performance. Train deal and operating teams to collaborate seamlessly across the lifecycle. And track and communicate the performance advantages relentlessly to sustain momentum. Transformation takes 18–36 months, but the advantages last far longer.

For firms unwilling to act, the consequences will be brutal. First in deal outcomes, as they lose to buyers who can execute better. Then in fundraising, as LPs consolidate commitments with managers who demonstrate real operating capabilities. And finally in survival, as the widening performance gap renders laggards irrelevant.

Private equity has faced inflection points before: the leveraged buyout wave of the 1980s, the institutionalization of the 1990s–2000s, the operational pivot after 2008. Each time, firms that adapted thrived. Those that didn’t disappeared. The integration of operating partners throughout the deal lifecycle is the defining evolution of this era.

The debate is no longer whether operating partners matter—it is when they matter. Post-close engagement is already too late. The firms answering “from the beginning” are pulling decisively ahead. The firms answering “after close” are falling permanently behind. The diligence integration imperative isn’t about incremental improvement—it’s about survival in a market that no longer tolerates operational mediocrity.